Many claim using cash is the reason why Envelope Budgeting is so effective. On Dave Ramsey’s website he states, “There’s something psychological about spending cash that hurts more than swiping a piece of plastic.” Does using cash create the effectiveness of Envelope Budgeting or is it in the power of “choice before one spends”? Can a digital envelopes system replicate the success of a cash envelopes budget system?

RELATED: What is the Cash Envelope System?

Cash vs Digital

Spending with cash creates an immediate awareness of transfer of ownership. One is truly trading the value of money for the value of something.

Can that same feeling be replicated digitally?

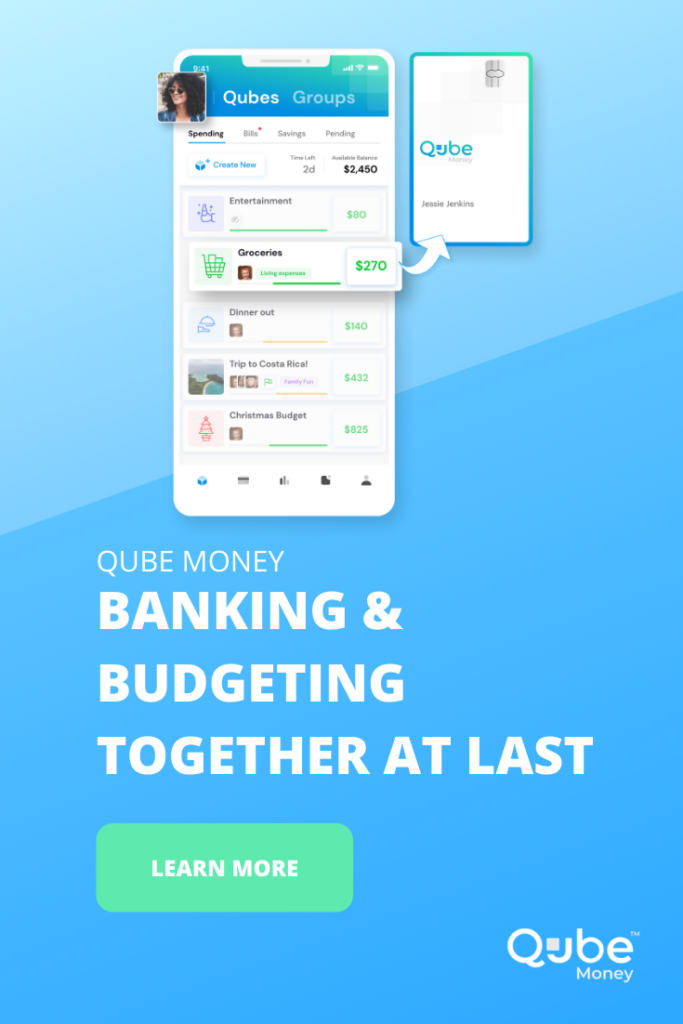

You tell me. Imagine digital envelopes connected to a default zero debit card.

When you deposit money into your bank account, the app enables you to split your money into your digital envelopes or virtual cubes. Every dollar has a job.

When you go to make a purchase, you open your app, view your envelope balances, and tap the envelope from which you want to spend. The dollar value in that envelope immediately becomes available on your debit card and you are ready to spend. No overdrafts. The card won’t allow a purchase to exceed the balance of the open envelope.

After each purchase, the card returns to default zero. Your new balance in your digital envelope reflects your purchase. And the transaction is ledgered. All of this happens automatically within seconds of the purchase. And if you want, it will notify those with whom you share your budget.

1. Before the purchase – It requires its users to think before they spend.

2. Intentional – The app gives money isolated jobs–purpose.

3. The bank is the budget – The simplicity of spending directly from the budget makes it real and easy to see the limits of money.

But is it the idea of holding money, which is paper, that causes that loss? No, of course not. It’s the fact that there was a feeling of ownership with that 20 dollar bill and an awareness of your purpose for that money. When you give money to the seller, the exchange creates a “tangible” feeling of loss of ownership and the satisfaction that you used your money for its intended purpose.

In contrast, swiping a card has no feeling of ownership or awareness since people generally do not even know how much money they have in the first place. Thus, there is no feeling of loss or satisfaction.

The Psychology of Real Cash

Related: When Money Isn’t Real

Existing budgeting systems make this problem worse because they are ancillary (or isolated and separate) systems to the bank account where the real digital money lives. What happens is that IF someone happens to have the discipline to look at their budgeting tool before the purchase, the internal conversation may go like this: “Shoot, I only have $500 in my new computer budget, but I know there’s $2,000 in the bank. I think I’ll spend the money. Maybe I’ll do better next month on my budget.”

There is no consequence and no accountability to the plan. Further, the budgeting system has no power to help the person stick to the plan. The entire environment of the dual systems enables failure rather than enabling success.

The power of Real Cash is that the bank and the budget converge into one. This environment now enables success. It eliminates the need for balancing the two systems or syncing 100 uncategorized transactions. It removes the chore of categorization and makes budgeting as easy as spending.

Qube Money’s qubes are filled with Real Cash– like with the cash envelopes budget.

![Everything You Need to Know About the Cash Envelope System [+ Sample Budget]](https://marketing.qubemoney.com/wp-content/uploads/2020/01/1-20-20-the-cash-envelope-system-blog2-440x264.png)

{kind=link}