![How to Make and Stick to a Budget [Free Download]](https://blog.qubemoney.com/wp-content/uploads/2020/07/shutterstock_226560994-1280x640.jpg)

Have you tried to make a budget before and failed? Has it made you lose confidence in the idea of budgeting? If so, you’re not alone. Learning how to make a budget and stick to it is a challenging—albeit worthwhile—skill to learn.

After all, it’s easy to call and cancel cable. It’s straightforward to call your car insurance company and ask for a discount. But when it comes to managing your spending and following a budget, it takes practice, patience, and grit to get it right.

It’s never too late to learn how to make a budget. Whether you’re a young single, or just a few years from retirement, you can learn how to make a budget and stick to it. By taking a few simple steps, making the most of new budgeting technology, and offering yourself grace, you can become an expert at budgeting.

>>> Download Now: How to Stick to a Budget [Free PDF]

Why is it so hard to stick to a budget?

Most people don’t learn how to make a budget in school. Unless your parents sat you down at the kitchen table and taught you how to list out your expenses and track them, this may be new to you.

Learning new things can be challenging, but most adults understand with time, practice, and a bit of curiosity, they can add a new skill to their toolbox. For example, imagine learning how to play an instrument as an adult. You wouldn’t expect yourself to instantly be the next Mozart, right?

Yet, for some reason, when it comes to budgeting, adults expect perfection right away. They hope to have the discipline immediately. They expect themselves to know everything there is to know about personal finance and budgeting when they’re starting on a journey to learn how to make a budget. That’s part of what makes budgeting hard to learn for many people.

Related: You Need a Budget: 6 Reasons to Start Today

You have to remember that companies spend billions of dollars a year on advertising designed to make you part with your hard-earned money. There are TV shows that glorify lavish lifestyles and make the rest of us feel like we’re missing out.

Add in a touch of boredom, wanting our kids to have more than we had, and easy access to credit, and it’s no wonder why it’s challenging to have financial discipline.

In many ways, when you decide to learn how to budget, you’re also committing to changing the way you think about money. You’re working against societal messaging that has normalized debt as part of the human experience.

Now that you know why it’s been hard to make and stick to a budget, you can forgive yourself for overspending in the past. Here’s a step-by-step guide on how to finally create a budget that works for you and your family.

How to Budget, Step 1: Find Your Why

Before we talk about the nuts and bolts of your budget, step one is to find your “why.”

There has to be a reason why this time is different from all the other times you tried to manage your finances. Maybe you’re sick and tired of living paycheck-to-paycheck. Or you had a baby, and you want to provide a nice life for your family. Maybe you lost your job, and you realized you need a larger savings account.

Whatever the reason, hold on to that feeling. Learning how to make a budget takes time, but if you have a strong why for doing it, it will be easier to stick to the plan.

If you need help figuring out what your why is, work together with your family to come up with one together. Maybe you want to become debt free to take your family on a memorable trip. Or you have a child starting high school, and together, you decide you want to send them to college debt-free.

Involving your family in the decision to make and stick to a budget can bring everyone together around a common goal.

Also, don’t be afraid to go big when it comes to your why.

Your why can be as significant as creating multi-generational wealth and ensuring that starting with you, your family never has to worry about money again. There’s no limit as to how big your financial goals can be.

As you move on to the next step of creating your budget, keep your why in mind. When it seems overwhelming, when it looks like you’ll never get ahead, envision yourself achieving those big, audacious goals, and it will help encourage you to stay on the path to financial success.

How to Budget, Step 2: List Your Income & Expenses

Now that you have your why, your reason for embarking on this journey, it’s time to look at the numbers.

Before you even write down a budget, it’s time to do research into your own spending. Ideally, you should look back at your last three months of spending, but even looking back at one month of expenditures is helpful.

When you look at your spending, write down the average amount you spent on big categories like food, entertainment, clothing, child care, and more.

Notice your trends and your habits. Notice if you tend to buy a lot from one place. For example, you might already know you have a Target addiction, but you might not realize how much you go through the drive-through to grab a coffee.

But remember, this is an information-gathering mission. It’s not to judge yourself for your spending or give yourself a hard time. All you’re doing is bringing awareness to your spending in order to create the most realistic budget for you. The more realistic your budget is, the better you’ll stick to it.

Once you know where your money goes, you can turn that information into budget categories.

Read: 13 Main Budget Categories and 3 You Don’t Want to Forget

Common budget categories include:

- Direct to Savings

- Giving/Tithe

- Mortgage/Rent

- Groceries

- Entertainment

- Eating Out

- Childcare

- Insurance

- Water

- Gas

- Electricity

- Internet/Cable

- Medical

- Medical Insurance

- Clothing

- Gifts

- Student Loan Payments

- Hobbies/Kid Activities

- Beauty/Haircuts

- Allowance/Fun Money

You can adapt your budget categories to fit your needs. Some people will have more categories than this list, while others may have less. That’s where your research comes in handy because it will show you how many categories you need and where you spend.

Next, write down your net income. Your net income is the money that hits your bank account when you get paid (vs. your gross income, which is what you get paid before taxes, insurance, retirement deductions, etc. are taken out.)

Divide your net income among your categories, like putting $400 in the grocery category, or $30 for gifts.

If you have money left over at the end, great! Assign extra money a job by allocating it to savings or to a big goal, like buying a house.

Read: How to Save Money in 2020

If you don’t have enough money to cover every category, it’s time to go back to the drawing board. What can you cut out to create more space in your budget? What ideas do you have to earn more money to cover all your expenses with room to spare?

How to Budget, Step 3: Start Using the Envelope Method

Now you know how to create a budget, but that’s not the hardest part. The biggest challenge for most people using a budget is sticking to the budget. If you’re new to budgeting, the cash envelope method is the easiest way to stick to a budget.

There are two main ways to use the cash envelope method. You can use physical cash envelopes, or you can use digital envelopes. Both methods are effective in helping you stick to a budget.

With cash envelopes, you would go to your bank or the ATM at the beginning of each budgeting period and withdraw the amount of money you want to spend. Create an envelope for each category and allocate the cash into each one.

When the cash is gone, you can’t spend any more. If you’re halfway through the month and you don’t have any grocery money left, it’s time to go shopping in your own pantry.

Related: 10 Reasons Budgeters Hate Cash Envelope Budgeting

Many people don’t like handling cash, and more and more vendors are starting to go cashless. Another way to use the envelope method is to use digital envelopes.

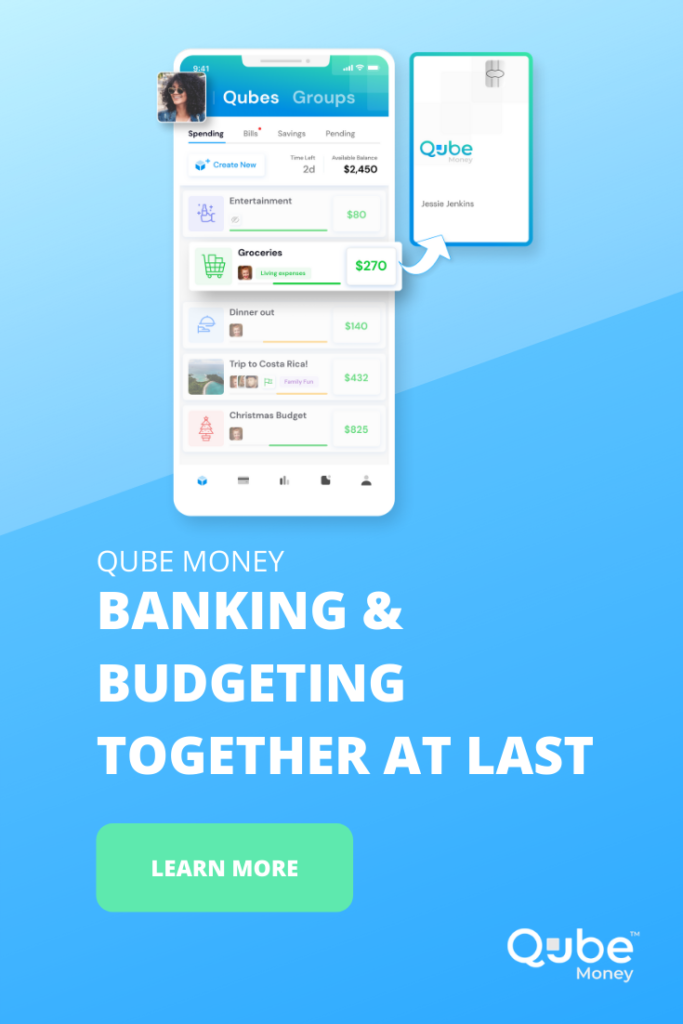

You can create digital envelopes using an innovative fintech app like Qube Money. With Qube, you can see all of your categories on your phone screen.

This video explains how it works.

Activate a category and then use your Qube card to spend. This helps you stay accountable and keeps you under budget. On average, when people spend using a debit card or credit card, they spend 17% more than intended. But, with Qube, you can use the convenience of a card without going over budget.

The envelope method works well because it helps to create discipline, reminds you of your goals, and shows you how much is left in each category.

Many people use the envelope method to start their budgets and stick to them. Now, thanks to the wonders of technology, you can bring the old school cash envelope method to your phone with Qube!

How to Prevent Budget Mishaps

As you get used to budgeting and using an app like Qube, you might notice that an unexpected expense will come up with some frequency. A small expense, like a birthday party. Other times, significant car repairs. These types of costs can ruin even the most carefully planned budget. One way to avoid those types of issues is to create sinking funds and an emergency fund.

Read: The 6 Biggest Money Mishaps a Budget Can Help You Avoid

An emergency fund is a savings account separate from your regular checking account. It’s not something you want to be able to access easily. In fact, you might want to keep your emergency fund at a different bank entirely.

The starting amount to keep in an emergency fund is $1,500. Eventually, though, you can get your emergency fund to cover 3-6 months of expenses. Having an emergency fund gives you great peace of mind and enables you to take care of life’s biggest messes.

If you have to buy a last-minute plane ticket to see a sick relative, you can do it using your emergency fund. If your water heater breaks in your house, you can fix it using your emergency fund.

Also, consider starting a few sinking funds. Sinking funds are small savings accounts for different events that come up or goals you may have.

You might want to start a sinking fund for Christmas, birthday parties, or a vacation. You can keep it in a savings account or an envelope you add to every month. When the holidays come around, you won’t break your budget by buying Christmas presents. You just go to your sinking fund and use that money to buy gifts.

Read: How to Budget for Periodic Expenses

With a combination of a solid emergency fund and sinking funds, you’ll be much better able to weather life’s financial surprises and stick to your budget once and for all.

Get Accountability

One last tip for sticking to a budget is to get accountability. If you don’t have a spouse to create a budget with you, ask a friend or family member to make their own budgets alongside you. You can also ask a friend at work to keep you accountable.

If you’re a more private person and prefer to work on your budget alone, make sure to check out support communities online. There are many bloggers, and Instagram accounts about budgeting. There’s a community called the debt-free community on Instagram (#debtfreecommunity) who root each other on when people are paying off debt.

Ultimately, there are many ways you can share your story and get accountability even if you want to remain anonymous. Remember, budgeting and sticking to a budget isn’t a sprint. It’s a marathon, and it’s helpful to have people cheering for you along the way to help you reach your goal.

Final Thoughts

Remember, if you’re a new budgeter, it’ll take time to learn how to do it effectively. Budgeting is a skill you can learn and improve upon over time. It takes anywhere from three to four months to get the hang of making a budget every month and sticking to it. It might also take you a few months to start saving an emergency fund and to get used to creating sinking funds.

But, over time, you’ll get on track financially. Don’t forget to ask for help when you need it and take advantage of new financial technologies like Qube Money, which can help you to stay on track and organized.

Also, don’t forget to reach out to friends and family to tell them what you’re doing. The more accountability you have, the more easily you’ll reach your financial goals and learn how to budget once and for all.

![Everything You Need to Know About the Cash Envelope System [+ Sample Budget]](https://blog.qubemoney.com/wp-content/uploads/2020/01/1-20-20-the-cash-envelope-system-blog2-440x264.png)

{kind=link}