Money can open doors to new experiences and opportunities, yet you may struggle with it. According to Northwestern Mutual’s 2018 Planning & Progress Study, 87% of survey respondents said that they’re most happy when their finances are in order. At the same time, money was also cited as a major cause of anxiety and stress.

Although money can be polarizing, you can create a healthy relationship with money. Here are a few ways to find balance and achieve a financially healthy life.

Financial Basics

A financial plan helps you prepare (as best you can) for what life throws in your direction. It shows you where you are today, reminds you of where you want your future self to be, and helps you identify how to get there. But to establish the framework for a financial plan, you’ll need to know a few things.

1. Decide on a Goal

When mapping out your financial situation, the first place to start is with an overarching goal. The best goals are S.M.A.R.T.

- Specific: Clear and well-defined.

- Measurable: Easily track progress toward your goal.

- Achievable: Attainable based on current circumstances.

- Relevant: Results-oriented, aligns with your overall objective.

- Timely: A target date to reach your goal.

For example, instead of the goal, “I want to save money,” your S.M.A.R.T. goal could look like, “I want to save $1,000 for my emergency fund in seven months.”

2. Calculate Your Income

Your income is one of the key players in understanding the parameters of your finances. It’s also the starting point you should be aware of to avoid overspending and the subsequent burden of repaying debt.

Although it’s a good idea to know what your gross income is, your net income is the amount you’ll work with on a day-to-day basis. Add up your total net income including earnings with your full-time job, side hustles, passive income streams, and other sources of regular income.

3. Know Your Total Expenses

You may be striving toward a goal (or two), but as you’re working toward your goals you’ll need to pay for a few essential expenses. These expenses are necessary to keep your finances in balance while keeping you out of the red.

Some examples of essential monthly expenses are mortgage or rent payments, utility bills, car payments, gasoline and insurance, groceries, personal hygiene goods, etc. Tally up the average cost for these crucial expenses to get a clearer sense of how much money you have leftover to allocate toward your other goals.

Mastering a Budget

The next step in setting yourself up for a financially healthy life is setting boundaries. When it comes to money, these boundaries come in the form of a budget.

4. Set a Monthly Budget

You now know how much money comes in and how much you’ve taken out of your bank account for monthly essentials. Now, it’s helpful to categorize your expenses and choose how much of your cash you want to commit to each category. For example, you may set a grocery budget, a dining out budget, or a clothing budget.

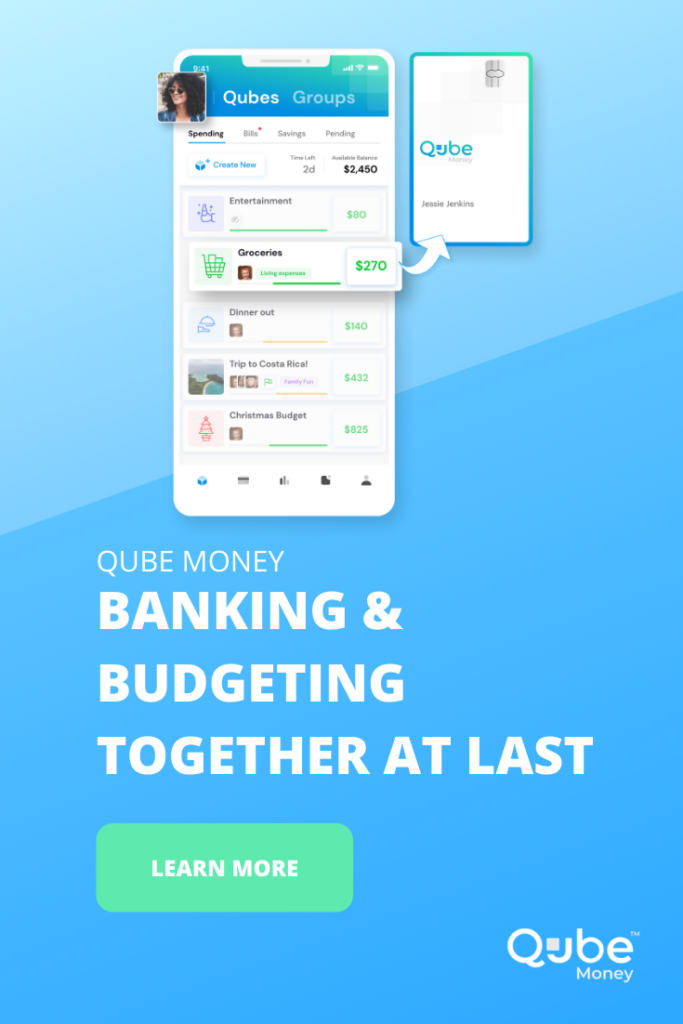

A powerful and convenient approach to tracking your budgets is through digital cash envelopes, or “Qubes” as we call them at Qube Money.

You can spend up to the amount in a qube’s budget. When you run out of funds, you must either stop spending toward that qube or make a deliberate choice to transfer funds from another qube. This is designed to help you avoid overspending, and instead, be intentional with your spending.

5. Do Routine Check-Ins

Life isn’t static — and your budget isn’t either. For example, in November, you might need to increase your grocery budget by $100, if you know you’re hosting Thanksgiving dinner.

Performing a regular budget check-in to see how well you were able to stay within a budget is crucial to your ongoing financial wellness. Constantly burning through a budget can make the idea of budgeting, in general, feel demotivating. But, the reason funds were used up so quickly might be a result of an unrealistic budget — not because budgeting doesn’t work.

By revisiting your budget, you can move necessary pieces of your finances around, like a puzzle piece, to ensure you’re handling your finances in a realistic way that fits your needs.

Tackling Debt

Debt can feel financially and mentally exhausting. First things first: stop adding to your debt. This means locking away credit cards and avoiding opening new loan accounts, if possible. Once you’re in a place that you’re not adding to your debt, you can find a repayment system that works for you.

6. Know Your Debt and Interest Rates

Before jumping into actionable ways to pay down your debt, it’s necessary to know your starting point.

Again, assuming you’re not taking on more debt, write down how much you owe for each credit card or loan, the interest rate for each one, and the minimum balance due each month. This information helps you track your debt and can help you achieve a financially healthy life.

7. Choose a Debt Repayment Method

Different debt repayment strategies are available to help you navigate your way toward debt-free finances. The two most popular debt repayment methods are the debt avalanche and the debt snowball.

Debt Avalanche

A debt avalanche is a practical approach to debt repayment. It asks you to focus any extra financial resources to pay off the debt with the highest interest rate first. Prioritizing the debt with the highest interest rate helps you pay off debt sooner and ensures you’re spending less money on interest over time.

It works by aggressively making higher payments toward the highest-interest debt while making minimum payments toward other debt. Once you’ve fully paid the highest-interest debt, the higher payments are paid to the next highest-interest debt until it’s paid off, and so on.

Debt Snowball

The debt snowball is a useful approach to gain small wins but may cost more money in the long run. Ultimately, the goal of this method is to keep you motivated on your debt repayment journey.

It works by aggressively making higher payments toward the lowest debt balance first while making minimum payments. Once that account is paid off, you’ll direct higher payments toward the next lowest debt balance until that account is fully paid, and so on.

There’s no “right” or “wrong” approach here — the goal is to eventually repay all of your debt. Choose an approach that resonates with you and that you feel confident you can stick to.

Paying Yourself First

All of these steps are to help ease the anxiety and stress of financial planning today. Setting up your future-self for a financially healthy life is key to maintaining balance during your retirement years, too.

8. Start Early

Saving for retirement, whether you’re setting money aside in an employer-sponsored 401(k) or have an Individual Retirement Account (IRA), is crucial to start as soon as you begin working. Interest earned in a retirement account compounds, meaning the interest earned in the account is re-invested so you continuously earn more interest over time.

Make sure you enroll in your employer’s 401(k) as soon as you’re eligible. If your employer doesn’t offer a retirement plan, you can open your own IRA through a bank, credit union, or online broker, like Betterment.

9. Maximize Employer Matching

Some employers match employee retirement contributions up to a certain percent as part of its benefits package and to incentivize employees to save for retirement. For example, your employer may match your contribution up to 5%. If you contribute 5% of your paycheck to your sponsored 401(k), your employer will contribute another 5%, raising the total contribution to 10% of your income.

If your employer does offer a retirement plan, ask your Human Resources department about retirement matching provided by the company.

Managing Financial Stress

Planning and managing a financially balanced life doesn’t happen instantly. It takes time to shed old money habits, and reframe your behavior and perspective about finances.

10. Take a Deep Breath

Scientific studies suggest that deep breathing can calm the brain, help maintain focus, and reduce anxiety. When we’re faced with a financial stressor, the body and mind are inclined to react — this may surface as stress eating, reckless spending, or outright denial and avoidance.

Taking 10 minutes to close your eyes and focus on mindful breathing can help you steady the strong emotions associated with money, and help you regain your bearings toward a clear, thoughtful, next step.

11. Make Time for Exercise

Achieving financial wellness is easier to accomplish when you’re maintaining your physical health. According to Psychology Today, studies found that aerobic exercise contributes to increased brain function, specifically improved memory, and thinking skills.

To help make physical health as much of a priority as financial health, try time-blocking one hour in your schedule to exercise a few days a week.

12. Remember It’s O.K. to Say “No”

Balance doesn’t mean agreeing to or saying “yes” to everything at once. In fact, doing so may mean a fast-track to burnout and being overwhelmed. Instead, narrowing down your to-dos and goals to the 2-3 tasks will yield the most impact. By reducing the distractions on your plate, you’re doing more toward your greater purpose.

13. Talk to Someone Who You Trust

You don’t have to go on this financial journey alone. Talking to someone about your financial challenges may help you better understand what approaches can or won’t work for your circumstances. This person may be a spouse, a parent, a long-time friend, a financial professional, or a therapist — regardless of who you invite to these conversations, make sure you feel you feel safe and comfortable trusting them, entirely.

We’ve shared with you 13 ways to live a financially healthy life. Now it’s your turn to go make it happen! To learn more about Qube Money visit our main page at www.qubemoney.io.

{kind=link}